Previous article

Previous article For Companies and Institutions

-

Commercial Banking

We provide credit, financing, treasury and payment solutions to help your business succeed. We also offer best-in-class commercial real estate services for investors and developers.

-

Global Corporate Banking

We help clients achieve their long-term strategic goals through financing, liquidity, payments, risk management and investment banking solutions.

-

Investment Banking

Providing investment banking solutions, including M&A, capital raising and risk management, for a broad range of corporations, institutions and governments.

-

Payments

Your partner for commerce, receivables, cross-currency, working capital, blockchain, liquidity and more.

Key Links

For Institutional Investors

-

Asset Management

Putting our long-tenured investment teams on the line to earn the trust of institutional investors.

-

Markets

Direct access to market leading liquidity harnessed through world-class research, tools, data, and analytics.

-

Securities Services

Helping institutional investors, traditional and alternative asset and fund managers, broker dealers and equity issuers meet the demands of a rapidly evolving market.

-

Global Research

Leveraging cutting-edge technology and innovative tools to bring clients industry-leading analysis and investment advice.

-

Prime Services

Helping hedge funds, asset managers and institutional investors meet the demands of a rapidly evolving market.

-

Global Liquidity Solutions

Global short-term fixed income strategies designed to help clients manage liquidity through the cycle.

Key Links

For Individuals

-

Wealth Management

With J.P. Morgan Wealth Management, you can invest on your own or work with an advisor to design a personalized investment strategy. We have opportunities for every investor.

-

Private Bank

A uniquely elevated private banking experience shaped around you.

For Employers

-

Workplace Solutions

Enhance your equity compensation offering with solutions designed to empower your employees and bring your reward strategy to life.

Key Links

Who We Serve

Key Links

All Insights

Explore a variety of insights.

Key Links

Insights by Topic

Explore a variety of insights organized by different topics.

Key Links

Insights by Type

Explore a variety of insights organized by different types of content and media.

Key Links

About Us

We aim to be the most respected financial services firm in the world, serving corporations and individuals in more than 100 countries.

Key Links

- Payments

- Payments Unbound

- Payments Unbound - The digital magazine

- Payments Unbound Articles

- Evolution & Future of Payment Rails (Visual Timeline)

X less

Featuring future-thinking clients

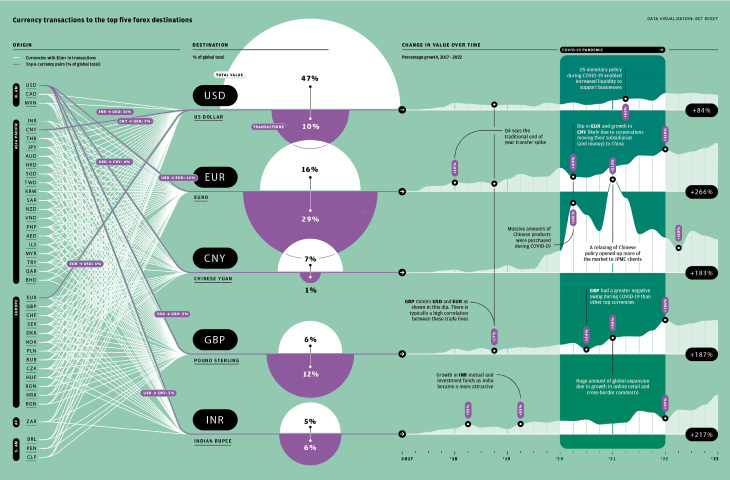

Payments Unbound unites clients from a wide range of industries to bring you innovative insights that help you navigate the future of payments.

Payments Unbound Volume 4 Payment Rails: A Visual Timeline

J.P. Morgan Payments

Tracking the evolution of payment rails

5 minute read

The world of payments is changing faster than ever

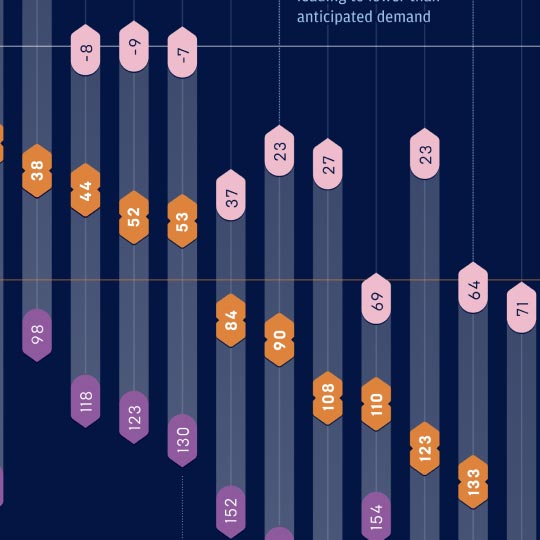

Visual timeline

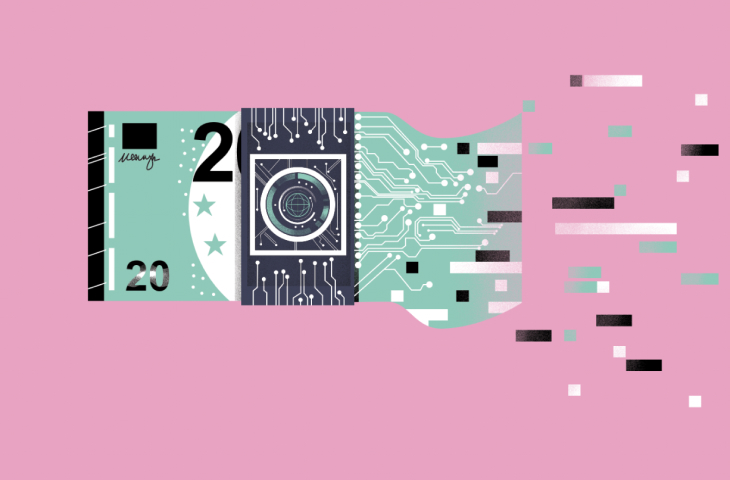

Payment rails are the underlying networks and infrastructure that enable funds to get from A to B without the transfer of physical money. They ensure that when a payment is initiated by one person or institution, it is received by the intended beneficiary. From wire transfers and cards to online transactions and real-time settlement, payment rails have experienced a dramatic evolution.

Bills of exchange

Before digital means of transferring money, there were analog mechanisms such as “bills of exchange.” These eventually evolved into modern-day checks.

1871

Wire transfer3

Before digital means of transferring money, there were analog mechanisms such as “bills of exchange”. These eventually evolved into modern-day checks.

1958

Card rails arrive4

Bank of America launched a consumer credit card offering revolving credit, the first of its kind. This evolved into Visa, and spawned a whole industry of credit cards.

1968

Automated clearing houses5

A clearing house is an organization that mediates the exchange of payments. The UK Bankers’ Automated Clearing System (BACS) was the first automated version.

1970

1978

Standardization of international transactions9

Swift, a cooperative of 239 banks from 15 countries, established a payments network with common standards for international transactions.

1997

Mobile payments10

The first mobile payments were made in Finland, when Coca-Cola introduced vending machines that enabled users to authorize payment by sending an SMS.

1999

2001

2009

Bitcoin was the first cryptocurrency. Operating through a distributed "blockchain" ledger that’s not owned by a single entity, it facilitates funds transfer without intermediaries.

2010s

2020

2024

Account-to-account (A2A) payments at point of sale

A2A payments are growing fast. In 2024, innovators are exploring how these can come to physical retail terminals.

Looking ahead

Artificial intelligence

From enhancing fraud detection to streamlining processes, AI will help existing rails deliver greater speed, security and cost efficiency.

By Wired

SOURCES: AS PER WIRED, MAY 2024

ILLUSTRATION: ADRIÀ VOLTÀI

MAGAZINE

Volume 5: Game Changer Volume 4: Ready Payer One Volume 3: Bank to the Future Volume 2: The New World of Commerce Volume 1: The Money Revolution Browse all articlesWEBINARS

View all webinars

You're now leaving J.P. Morgan

J.P. Morgan’s website and/or mobile terms, privacy and security policies don’t apply to the site or app you're about to visit. Please review its terms, privacy and security policies to see how they apply to you. J.P. Morgan isn’t responsible for (and doesn’t provide) any products, services or content at this third-party site or app, except for products and services that explicitly carry the J.P. Morgan name.