Previous article

Previous article

WIRED REPORTS

What will be the most significant shift in credit over the coming decade?

5 minute read

Credit has been a crucial part of our everyday lives for decades.

TWO SIDES OF THE SAME COIN

But over recent years, a wave of technological innovation— big data, algorithms, machine learning—have brought about notable changes. The credit marketplace has expanded, welcoming a raft of startups and new kinds of agile credit products designed to suit new kinds of borrowers. This has spurred traditional financial institutions to evolve, while for regulators it has posed new questions. In this moment of flux, many are wondering: What will the future hold? We asked two experts for their takes on two megatrends...

The rise of “buy now, pay later”

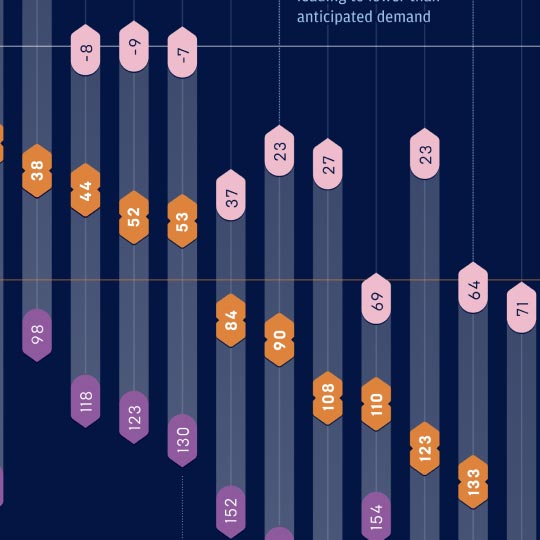

‘Buy now, pay later’ (BNPL) enables consumers to stagger the cost of a purchase over an agreed period of time, often with no fee or interest. Instead, the BNPL provider’s revenue mostly comes from taking a percentage of the purchase—and retailers have jumped at the proposition. According to Insider Intelligence, based on current trends, BNPL will account for $680 billion in transaction volumes worldwide in 2025.

Though the explosion of BNPL began during lockdown, it’s already evolving again, and we can expect to see more expansion into new categories. You can find BNPL options for rent, gas, even groceries. In the future it may also become more common in physical shops, particularly for mid- and high-ticket items, because it increases basket size and conversion rates.

As this develops, we can expect BNPL providers to increasingly offer accounts with virtual cards for consumers to store in their digital wallets. That would mean consumers can just tap their device on the terminal at any checkout where that particular provider is accepted. This is already happening in the UK, Australia, and New Zealand.

The rise and maturity of BNPL will spur innovation in traditional credit offerings. Banks are already integrating BNPL features into their credit card programs, particularly to appeal to younger customers. I also expect to see the growth of various hybrid-type credit products so that their customers aren’t restricted to specific retailers.

It’s not all good news for BNPL providers, however. The ability to offer zero percent interest relies on a low interest rate environment, as BNPL providers often need to borrow to fund their operations. If interest rates continue to rise, these models will become harder to sustain.

Then there’s future regulation, which will require BNPL providers to carry out the same kind of affordability checks as banks. This will be good for consumers, and probably for the long-term sustainability of the industry. However, it will significantly reduce the revenues of those whose models depend heavily on customers paying fees for missing a periodical payment. This may provoke some to move from an interest-free to a low-interest offer, even if this is a harder sell.

Each type of credit comes with its own nuance. BNPL has its benefits for many customers compared to higher cost alternatives, but first it must overcome these pressing existential challenges around its long-term business model and ensure it meets new regulations.”

New data sources expanding access to credit

“Lenders have traditionally calculated a potential borrower’s credit score by reviewing their record of repaying loans in the past. But this data doesn’t exist for everyone. In the United States alone, more than 50 million people have a thin or nonexistent credit history.

Relying solely on a customer’s traditional credit history can leave broad swaths of the population unable to access financial products, such as credit cards, mortgages, or even straight-up loans.

This is why expanding the types of data used to make decisions is so important. Machine learning and expanded data can create a holistic view of a potential borrower’s ability to repay a loan, even without a traditional credit history.

Recurring payments for such items as utilities, cell phones, and rent have not traditionally been included in a consumer’s credit history, and for this reason their responsible history for making such payments could not positively impact their credit score. Until recently, there has also not been a sound mechanism for the ongoing reporting of these positive payments because there has been no requirement to report them to the credit bureaus.

As technology develops, so do the possibilities for consumers. Our product Experian Boost enables customers to raise their credit scores by self-reporting payment data for Netflix subscriptions, cellphones, utilities, and more. Since it was launched, four years ago, 90 million points have been added to scores and the average consumer gets a 13-point increase through the platform.

Our internal analysis demonstrates that these categories of payment, which show a continuous commitment over time, are predictive of future credit risk. That’s exciting because as our digital footprints grow, there will be millions of new data points that can potentially be incorporated into evaluations to help expand access to credit. The future is about broadening into data across more categories, and enabling consumers to choose which data they share and when.

Advancements in technology will enable us to analyze this data more accurately, paving the way for lenders to expand their business by extending credit to more borrowers without assuming more risk. It also promises a future of greater financial inclusion, because low-income communities and communities of color have been disproportionately affected by limited credit histories. Leveraging expanded data sets and tools enables us to welcome previously underserved consumers into the mainstream lending economy.”

BY WIRED

SOURCES AS PER WIRED, AUG 2023

PROFILE ILLUSTRATION: ADI GILBERT