Previous article

Previous article

J.P. Morgan Payments

Tectonic shifts

5 minute read

The world of payments is changing faster than ever

TRENDS WATCH

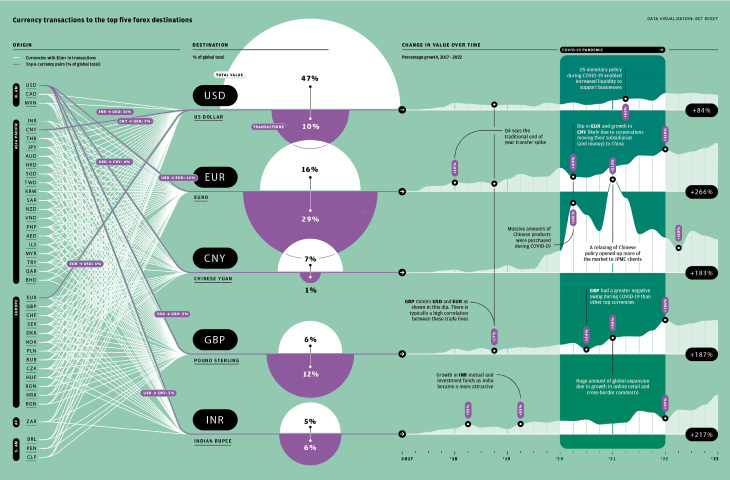

Globalization has been under pressure in recent years. The Covid pandemic and geopolitical conflict have led companies to relocate supply chains to countries or build supplier networks closer to home. Some countries have also been imposing export restrictions on vital goods such as food, fertilizer, and raw materials. According to the International Monetary Fund (IMF), the number of trade barriers introduced each year has tripled since 2019.

However, despite the headwinds, the world is not atomizing. New trade patterns, new relationships and new markets are emerging. Payments innovation will play an important role in easing these changes, making businesses more efficient and agile, reducing the cost of transactions, and supporting the frictionless movement of money across borders. Here is a closer look at some of the major payments trends that are happening around the world right now...

1

Latin America

Near-shoring becomes big business

Global instability has led to growth in near-shoring, whereby companies move supplier networks close-by. The U.S. for example is looking to Mexico as an alternative and less risky manufacturing location. Mexican near-shoring generated some $30 billion in foreign direct investment in the country in 2022, according to Credit Suisse. Central America, which has strength in the garment industry and increasingly in auto parts, is also seeing growth as a U.S. outsourcing option. Manufactured goods from South America can reach U.S. ports in a matter of days, compared to weeks for cross-Pacific shipping. As U.S. companies adapt their logistic strategies, innovative forms of supply chain finance will emerge—the volatility of various currencies in Latin America means some trade finance loans may need integrated FX-hedging. And, if businesses split their supply chains between countries, it will require cross-border payments, often in currencies they haven’t dealt with before.

2

North America

A hub for omnichannel experiments

Digital payments in the U.S. are expected to hit a total value of $3 trillion in 2024, more than double that of 2020, according to Statista. This rapid growth is partly being driven by retailers offering more integrated omnichannel experiences: Payments solutions that work across all touchpoints, from point-of-sales terminals to smartphones, online stores and marketplaces. New technologies which reduce friction at checkout and improve security are helping spur the omnichannel trend. Biometric authentication, such as palm scanners or facial recognition, is gaining traction; Amazon-owned Whole Foods recently announced its adoption of palm recognition tech nationwide1. Similarly, restaurant chain CaliExpress is implementing pay-by-face technology powered by PopID2. The FedNow real-time-payments (RTP) infrastructure, launched in 2023, will accelerate this shift. The scheme allows consumers and businesses to make instant payments from their bank accounts, at any time, and will greatly reduce usage of cash and checks.

3

UK & Europe

Open banking lays the groundwork for A2A

The European Union’s second Payment Services Directive (PSD2) was introduced to help grow innovations such as open banking, which required banks to develop standard ways to share transaction data with fintechs and other third parties. Under open banking, payment initiation service providers (PISP) are permitted to transfer money straight from a consumer’s account to a merchant’s—the basis for account-to-account (A2A) payments. A2A is promising because it cuts out intermediaries, making payments faster and cost effective. The UK in particular is looking at ways to promote A2A. Despite leaving the EU, the UK is a pioneer in open banking; today, more than one in seven British consumers use such services3. As the EU continues to make progress with open banking and real time payments, the European region could become a hub for A2A payments technology, bolstered by the expansion of the EU’s SEPA Instant scheme, which allows payments to be settled within ten seconds.

4

MENA countries

The rise of in-house banks

Major companies in the Middle East and North Africa (MENA) are looking to create in-house banks to simplify their accounts payable processes and reduce costs. The complexity of their current set-ups is partly a product of strong growth and international expansion. For firms operating across the many countries of MENA, it can be common to have hundreds of accounts spread across different banks. This results in complex payments processes, with varying reporting formats for different banks, while holding numerous accounts can result in high fees. In-house banking has the treasury operating a single account and centralizes key functions like account management, multi-currency payments, and cash consolidation. The number of physical bank accounts is then reduced by replacing them with virtual equivalents, which reduces expenditure. Plus, the centralized structure of an in-house bank can provide real-time visibility over cash balances.

5

APAC countries

Generative AI is set to transform treasury

Companies in Asia-Pacific (APAC) will triple spending on generative artificial intelligence (GenAI) to $3.4 billion in 2024, according to Infosys. GenAI is a category of machine learning that can analyze huge volumes of data based on plain language prompts and output text or visuals. Research suggests that East and Southeast Asia leaders in digital finance4, and treasury teams, will be fast adopters of this technology. With GenAI tools, treasurers will be able to upgrade the speed and quality of their data management. A simple prompt such as, “Do we have enough liquidity for the week?” could not only produce a rapid answer, but also relevant graphs and context. This would allow non- programmers to interact with complex data sets. Beyond ad hoc analytics, GenAI could also be used to routinely parse huge volumes of data to identify errors and anomalies, helping with account validation and fraud management, which are both long-standing treasury challenges.

MAGAZINE

Volume 5: Game Changer Volume 4: Ready Payer One Volume 3: Bank to the Future Volume 2: The New World of Commerce Volume 1: The Money Revolution Browse all articlesWEBINARS

View all webinarsMORE

Download a copy of volume 5 Get a physical copy of volume 5 Become a featured client J.P. Morgan Payments