Previous article

Previous article

J.P. Morgan Payments

Money’s new need for speed

5 minute read

Data viz

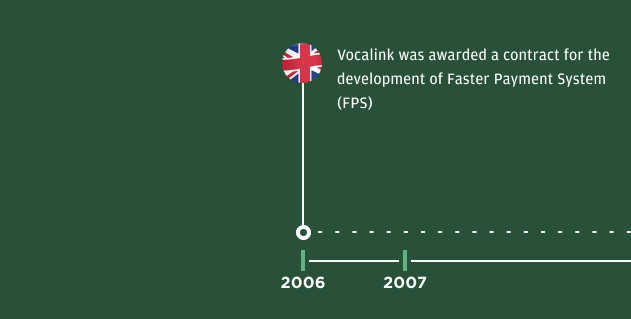

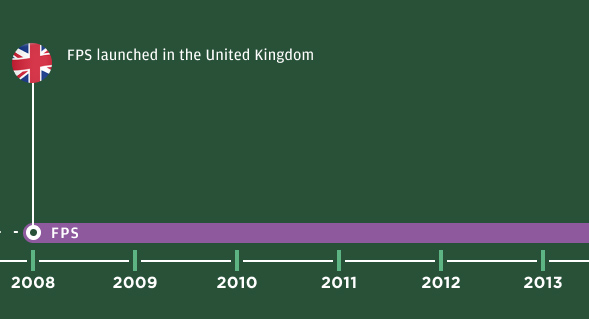

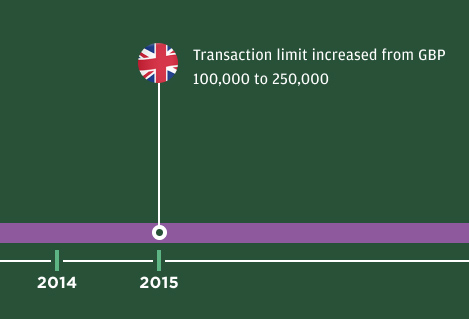

In 2008, the UK blazed a trail. That was the year when it launched its Faster Payments System (FPS), designed to streamline smaller business-to-business and bank-to-bank transactions. But its timing—at the very beginning of the smartphone revolution—meant that the FPS underpinned a far bigger shift in the digital economy1. Today, millions of individuals and businesses in the UK use the near-instantaneous settlement system to pay for goods and services online and in-person, often using their smartphones as the conduit.

Over the past decade and a half, more than 50 other markets have put in place their own real-time payments systems2, looking to create infrastructure that reduces the friction of digital payments, and which creates a solid platform for technology companies, from small startups to massive global businesses, to build out their own services and tools.

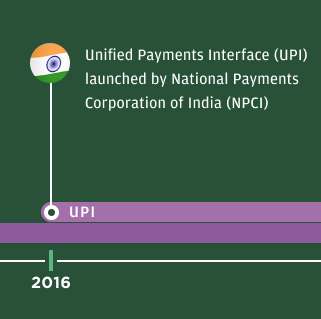

Despite the benefits of real-time payments, merchants haven’t always jumped to adopt it. In markets where payment cards are ubiquitous, brick-and-mortar and digital retailers don’t necessarily see an immediate need to add new payment methods. But in some markets—such as India, where the UPI real-time payments system is becoming the preferred mode for low-value transactions—merchants are highly motivated to start using real-time payments infrastructure. In those markets, where card penetration is low, real-time payments systems offer an alternative to cash3, 4.

Transacting at speed does create risks. Real-time payments are quick and irrevocable, making them easier for fraudsters to exploit than slower transfer systems. Authorized push payment (APP) scams— where a fraudster convinces an individual to send them an instant payment by pretending to be a legitimate business, friend, or love interest—have risen since the adoption of real-time payments. In 2022 alone, £485 million ($616 million) was stolen in the UK via APP fraud5. Customer awareness and consumer protection rules are catching up, but this fraud presents a huge challenge for governments, consumers, banks, and payment companies.

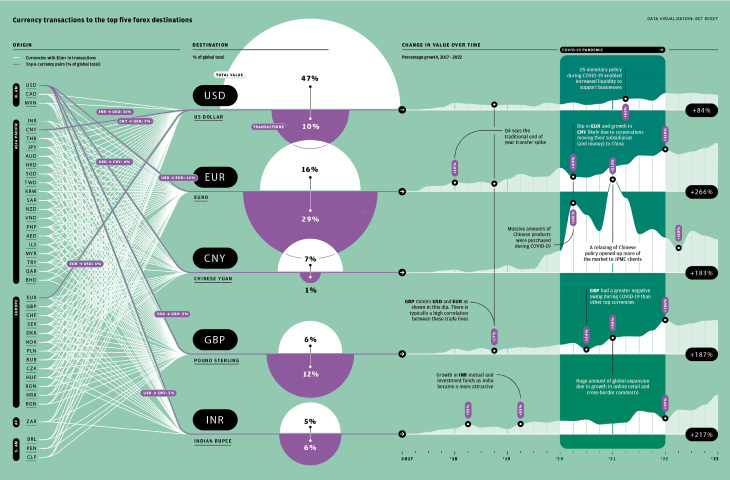

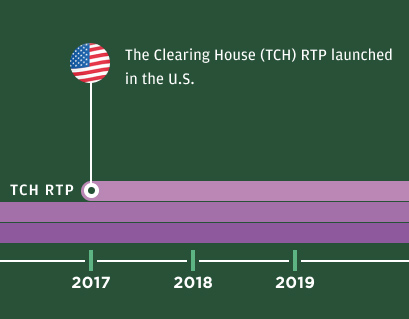

Still, the global real-time payment infrastructure is only going to continue growing. The U.S. Federal Reserve launched its FedNow service in July 2023, transforming the payments business in the world’s largest economy6. And with new data standards, such as ISO 20022, which will allow greater interoperability between financial institutions and payments networks, real-time payments are likely to increasingly cross borders. In this infographic, we explore the state of play right now...

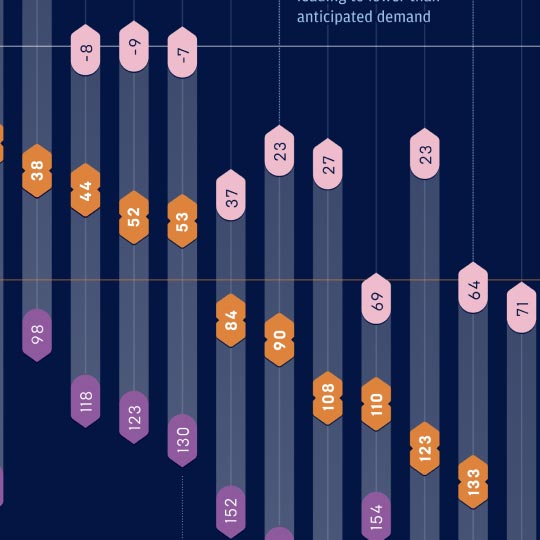

The U.S. sees real-time payments as new, compared to other markets with more widespread adoption

2nd

in Transaction

volume

volume

233.3

Billion transactions, 202230th

in Real-time

payments

payments

1.2%

of all transactions, 2022

Unified Payments Interface (UPI) enabled India to become the world’s largest real-time payments market

3rd

in Transaction

volume

volume

199.6

Billion transactions, 20222nd

in Real-time

payments

payments

44.6%

of all transactions, 2022

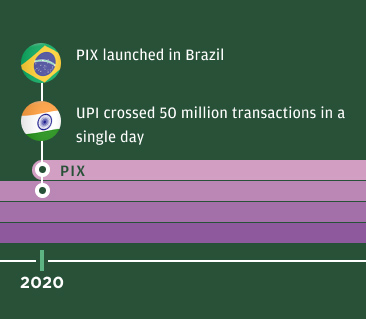

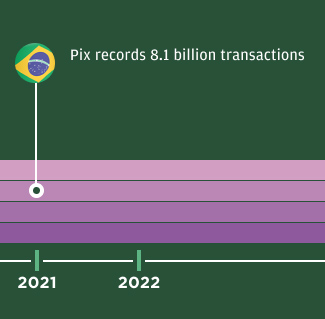

Pix revolutionized payments in Brazil, transforming customer behavior

4th

in Transaction

volume

volume

181.4

Billion transactions, 20225th

in Real-time

payments

payments

16.1%

of all transactions, 2022

The UK was an early adopter in real-time payments with the launch of Faster Payments System (FPS)

14th

in Transaction

volume

volume

39.6

Billion transactions, 202210th

in Real-time

payments

payments

10.1%

of all transactions, 2022Sources: ACI Primetime 2023, FIS The Global Payments Report 2023

Brazil

Brazil’s ‘Pix’ real-time payments network has strong branding and is free for certain P2P payments, boosting adoption.

14.2

India

India’s UPI real-time payments system is one of its most popular payment methods due to high adoption, ease of use, and cost-effectiveness.

7.4

United Kingdom

Real-time payments are significantly cheaper than traditional retail payment methods.

5.9

United States

The Clearing House RTP—reaches 67% of U.S. DDA accounts nationally FedNow Service—is expected to include many small banks, increasing financial inclusion

0.9

Future real-time payment adoption plans

USING NOW

Planning to use

Real-Time Payment Predictions

Sending

Receiving

Private organizations

Public organizations

MAGAZINE

Volume 5: Game Changer Volume 4: Ready Payer One Volume 3: Bank to the Future Volume 2: The New World of Commerce Volume 1: The Money Revolution Browse all articlesWEBINARS

View all webinarsMORE

Download a copy of volume 5 Get a physical copy of volume 5 Become a featured client J.P. Morgan Payments