Previous article

Previous article

J.P. MORGAN REPORTS

What’s the buzz in EMEA?

5 minute read

Europe, the Middle East and Africa are proving fertile grounds for innovation...

REGIONAL TRENDS WATCH

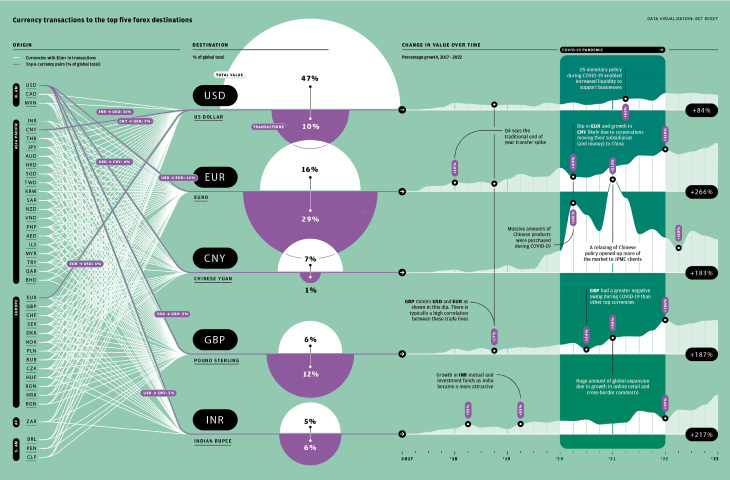

Europe, the Middle East and Africa (EMEA) comprises a diverse set of countries with a multiplicity of cultures, business environments and consumer preferences. What unites the whole region, however, is that payments innovation is typically driven by regulation. To navigate this diverse ecosystem, and the challenges and opportunities it presents, it is therefore essential to understand those regulatory drivers and the payments themes that are taking shape in response.

Click on a number below for more information on each country

2. UK

Digital money gains momentum

The concept of Central Bank Digital Currency (CBDC) continues to gain momentum in the UK, with the Bank of England recently publishing a consultation paper on a potential digital pound, written in conjunction with HM Treasury. The focus will now move onto a design phase over the next two to three years, which will examine the technology and policy requirements, and seek input from the public.

This is happening in parallel with CBDC activity on the continent. The European Commission published a proposed legal framework for a digital euro on June 28th 2023, and the European Central Bank is leading reviews to determine how a digital euro could be designed, distributed and regulated.

1. Netherlands

“PAY BY BANK” GOES INTERNATIONAL

In the Netherlands, 70 percent of e-commerce payments are by bank-to-bank transfer (a.k.a. “account-to-account”) via the iDEAL system, a sign of what can be achieved through the combination of open banking and instant payments. In 2023, iDEAL was acquired by the European Payments Initiative (EPI). This association of 16 different European lenders wants to create a pan-European payments system, and the acquisition heralds the potential for the development of a cross-border account-to-account network.

3. Saudi Arabia

Leading the Middle East in real-time payments

The Middle East is now the fastest-growing RTP market in the world. RTP transactions are expected to increase at an annual rate of 30.6 percent between 2022 and 2027, reaching a value of $2.6 billion. This is being driven by Saudi Arabia, which is attempting to modernize its payments infrastructure and increase the adoption of digital payments as part of its 2030 Vision. With around two-thirds of the Saudi population currently under the age of 25, digital wallet usage is already high, and by 2027, it is estimated that the majority of payments in the Kingdom will be electronic.

4. Germany

Watching the development of PSD3

Open banking is booming in Germany. According to analysts, it has the highest number of third-party providers (TPPs) in continental Europe. These are the companies that use APIs to access customer bank account information in order to provide commercial services. The sector is watching closely, therefore, as the European Commission moves to update its laws governing digital payments. The upcoming Payment Services Directive 3 (PSD3) framework has ambitious, wide-ranging goals, including “improving the functioning of open banking”. In practice, it will almost certainly require banks and financial institutions to move towards standardized APIs, improving quality and accessibility.

5. Brussels

European Lawmakers say yes to digital ID wallets

The European Parliament has voted in favor of creating a European Digital Identity (EUDI) wallet, where citizens can store IDs, health cards and other documents in a smartphone wallet. The goal is to have a digital ID solution available for 80 percent of the population by 2030 (approximately 350 million people). Use cases include payment verification and opening bank accounts, among many others. This will build on the groundwork done by local solutions such as DigiD in The Netherlands and SPID in Italy, and is considered an important step towards creating a digital ID card in the region.

6. Nigeria

In Nigeria, 63 percent of all point-of-sale transactions were conducted in cash in 2022. Yet e-payments are rising fast, driven by the wide availability of mobile phones. Electronic payments revenue is now growing by 35 percent per year, the fastest across the continent. Other African countries are also rapidly following suit, with the continent’s domestic e-payments market expected to grow 20 percent per year until 2025. This compares to a global revenue growth in e-payments of seven percent. What’s more, growth is set to remain high for the foreseeable future, as electronic and digital payments still account for only five to seven percent of payments in the region.

Click below for more information on each country

Could its real-time payments system go global?

India’s Unified Payments Interface (UPI), which allows instant peer-to-peer and person-to-merchant payments via mobile devices, is fast expanding internationally through partnerships in several countries including Singapore and the UAE. The National Payments Corporation of India (NPCI) is also enabling UPI capabilities using phone numbers for accounts in India held by Indian residents residing overseas. Developed by the NPCI in 2016, UPI is a major reason that India leads the world in real-time payments (RTP) – an estimated eight billion RTP transactions happen every month. The country’s central bank also recently launched India’s Central Bank Digital Currency (CBDC), the digital rupee. While still in its initial stages, a digital rupee on an interoperable blockchain can help facilitate real-time cross-border transactions without intermediaries and usher in an era of cheaper, more efficient currency management.

Moving towards digital currency

With the expansion of the digital renminbi or ‘e-CNY’ pilot for retail users in 23 cities in 2022, China became the largest economy to offer a Central Bank Digital Currency (CBDC) at scale. Users are now able to access their e-CNY in wallets on mobile apps. In parallel with the launch, the country’s popular online platforms are now allowing for e-CNY as a method of payment. Supported by the country’s existing retail payment infrastructure, the e-CNY system will help bolster China’s digital economy through a more secure form of currency, enhance financial inclusion, and drive greater efficiency. e-CNY has so far been used primarily for domestic retail payments, but there is potential for adoption across corporate and personal businesses in the near future.

EXPANDING RMB TREASURY CAPABILITIES

A major international financial center in Asia, Hong Kong serves as an important gateway to mainland China and is the largest center for conducting offshore renminbi (CNH) financing activities. As the renminbi (RMB) grows in popularity as an international payment currency, there is increasing demand from both foreign multinationals and China headquartered companies for CNH payments capabilities, such as flexible CNH FX rate optimization. The city’s central bank is also committed to expanding RMB liquidity in the region through enhancements to the RMB Liquidity Facility, as well as introducing additional risk management products such as Swap Connect.

BLOCKCHAIN IS ENABLING INNOVATION

Singapore continues to make strides when it comes to pioneering innovative ideas across the payments ecosystem. In 2016, the Monetary Authority of Singapore (MAS) along with industry players including J.P. Morgan, began experimenting with blockchain under the banner ‘Project Ubin’. Over five years, this explored how distributed ledger technology (DLT) could be used in everything from decentralized netting of payments to the ‘delivery-vs-payment’ (DvP) settlement process commonly used for securities. The success of this work is paving the way for commercialization such as a joint venture among DBS Bank, J.P. Morgan, Temasek and Standard Chartered which plans to operate a blockchain based, multi-currency clearing and settlement platform called Patrior. Now, the MAS continues to work on key initiatives to further advance DLT usage such as instant cross-border exchange and settlement of foreign currency transactions, as well as the programmable digital Singapore dollar. Current work on decentralized finance (DeFi) applications looks at how tokenized government bonds, Japanese yen and Singapore dollar deposits can demonstrate new models of trading, clearing and settlement.

NEW IDEAS CHANGING CASH DOMINANCE

Despite a plethora of digital payment choices in addition to credit and debit cards, cash remains the dominant medium of exchange in Japan. That is likely to change as the authorities have introduced a “Cashless Vision”with an aim to increase cashless transactions to 40 percent by 2025. To help achieve its goals, the Japanese government is set to introduce a system that will allow companies to pay a portion of salaries into e-wallets on mobile devices by spring 2023, alleviating the need to draw cash from ATMs. Such convenience coupled with discounts offered by these new payment providers will likely help drive the shift towards a cashless society. The transition to cashless payments is also expected to help overseas workers receive salaries without needing to open bank accounts, further expand financial services innovation in the market, and promote growth.

ALTERNATIVE PAYMENTS METHODS SURGE

The digital payment landscape in Australia and New Zealand has undergone significant changes in recent years. Cash and checks have been largely replaced as major forms of payments, with digital alternatives such as e-wallets, real-time peer-to-peer transfers and ‘buy now, pay later’ (BNPL) services achieving mainstream adoption. According to the Australian Treasury, almost half of the country’s population today make contactless payments using mobile and wearable devices. Real-time payments, launched in 2018, already account for a third of total peer-to-peer payments, and there are more than five million active BNPL users today. The trend towards a more digitized payments ecosystem is only expected to grow, driven by the rise in e-commerce, high mobile penetration and changing consumer behaviors that favor more instantaneous as well as convenient forms of payments.

One driver is new technological standards. The UK, South Africa and Switzerland, for instance, have all migrated to ISO 20022, and the Eurozone has expanded its existing use. This standard aims to move towards one common language for payment messaging, and enrich the data in payments messages for better, faster and more secure processing.

Another trend is the new series of regulations and initiatives in the Middle East that are enabling incredible progress towards real-time payments (RTP), with Saudi Arabia, Bahrain and the UAE leading the way.

And then there are the regulations relating to local programs such as UK Faster Payments and the Single Euro Payments Area, which are evolving as digital retail places ever-greater emphasis on the seamless secure processing of payments. For example, the UK has recently quadrupled its faster payments limit from £250,000 to £1 million.

Payments innovators within EMEA approach this fast changing landscape with expertise, curiosity, and a clear belief that payments can deliver more value tomorrow than ever before.

J.P. MORGAN PAYMENTS

FOR FURTHER DETAILS CONTACT YOUR J.P. MORGAN REPRESENTATIVE

SOURCES: WWW.JPMORGAN.COM/PAYMENTSUNBOUND/SOURCES

ILLUSTRATION: MANUEL BORTOLETTI