Contributors

Global Investment Strategist

Giving thanks

2024 has been a year for the books. As we close in on its final weeks, we at J.P. Morgan thought it would be timely to practice some Thanksgiving gratitude and reflect upon the past 11 months in markets.

So, before we get to the celebrations – and most importantly, the food – let’s dig into the three things we (and markets) are grateful for this holiday season.

3 things we (and markets) are grateful for this season

1. Answers to some of 2024’s biggest questions. While navigating uncertainty comes with the territory of being an investor, we acknowledge that both embracing it and forging ahead can be a tall order. Luckily, we are heading into year-end with some of 2024’s biggest questions already answered. We think that is definitely something to be grateful for:

- Could the Fed achieve a soft landing? Concerns about “too little, too late” swirled this summer as investors worried that labor market heart burn was a result of too aggressive tightening from the Fed. At the end of the day, it appears that despite some turbulence on the way, a soft landing may soon be reality for the Fed. The core measure of PCE inflation, which excludes food and energy, has fallen by three percentage points since its peak in 2022. That is quite the feat: Outside of wartime, the U.S. has never seen such a significant decline in inflation occur without a recession. This has all taken place without cracking the labor market, so far. While there is work to be done as policy rates continue to normalize, the direction of travel appears to be positive.

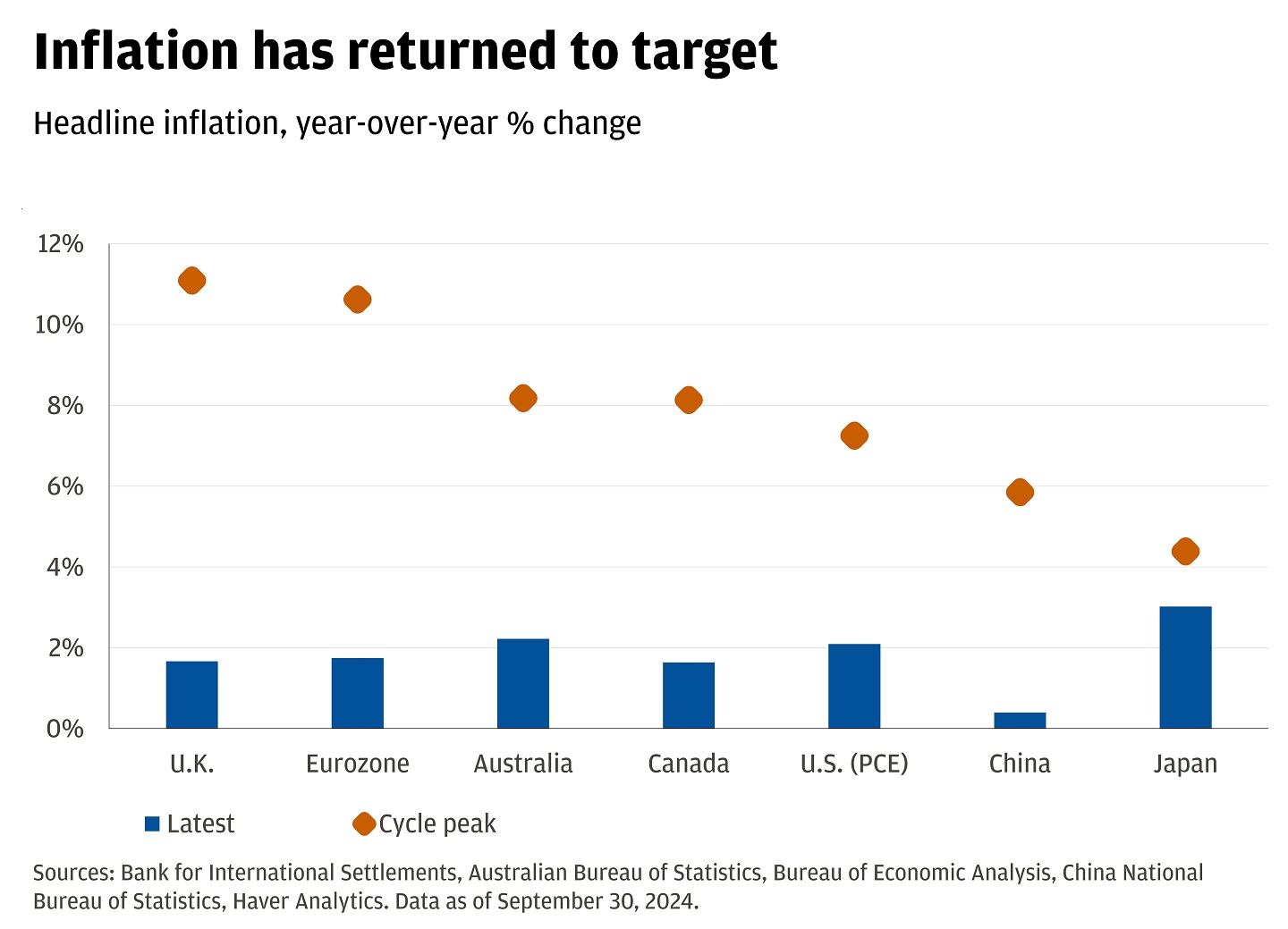

- Were global central banks actually ready to cut policy rates? Central bankers across the globe spent much of the past two years running historic tightening campaigns against excessively high inflation. This year was all about determining if they had in fact succeeded at their job (with added bonus points for doing so without causing cracks in the broad economy). Fast forward to today, inflation across the globe has fallen meaningfully toward policy targets. That gave the majority of policymakers the go-ahead to make the long-awaited pivot to ease. Of the 37 global central banks that we track, 27 are cutting policy rates, including every major central bank besides Japan. We think this gradual and coordinated global effort is set to continue and ultimately drive growth forward from here.

Inflation has returned to target

Headline inflation, year-over-year percentage change

This bar chart shows headline inflation year-over-year % change, with the latest values and cycle peaks shown. For the U.K., latest inflation was 1.7% and cycle peak was 11.1%. For the Eurozone, latest inflation was 1.7% and cycle peak was 10.6%. For Australia, latest inflation was 2.2% and cycle peak was 8.2%. For Canada, latest inflation was 1.6% and cycle peak was 8.1%. For the U.S. (PCE), latest inflation was 2.1% and cycle peak was 7.2%. For China, latest inflation was .4% and cycle peak was 5.8%. For Japan, latest inflation was 3% and cycle peak was 4.4%.

Source: Bank for International Settlements, Australian Bureau of Statistics, Bureau of Economic Analysis, China National Bureau of Statistics, Haver Analytics. Data as of September 30, 2024.

- Who would win the 2024 U.S. Presidential Election? We spent much of the first 11 months of 2024 (and before) talking about the election: from what history can tell us about market volatility leading up to and following elections to analysis of proposed policies from each candidate. Now that the dust has settled and Donald Trump is officially President-Elect, we have more clarity about what may be on the road ahead. While policies are yet to be confirmed, we are expecting the incoming administration to deliver trademark Republican pro-growth policies. Markets seem to agree; we have seen a sharp rally in both U.S. large-cap and small-cap stocks. Looking ahead, post-election clarity has historically been a powerful force for markets: Since 1984, there’s only been one election year when the market was lower 12 months after the election – in 2000, during the tech bubble.

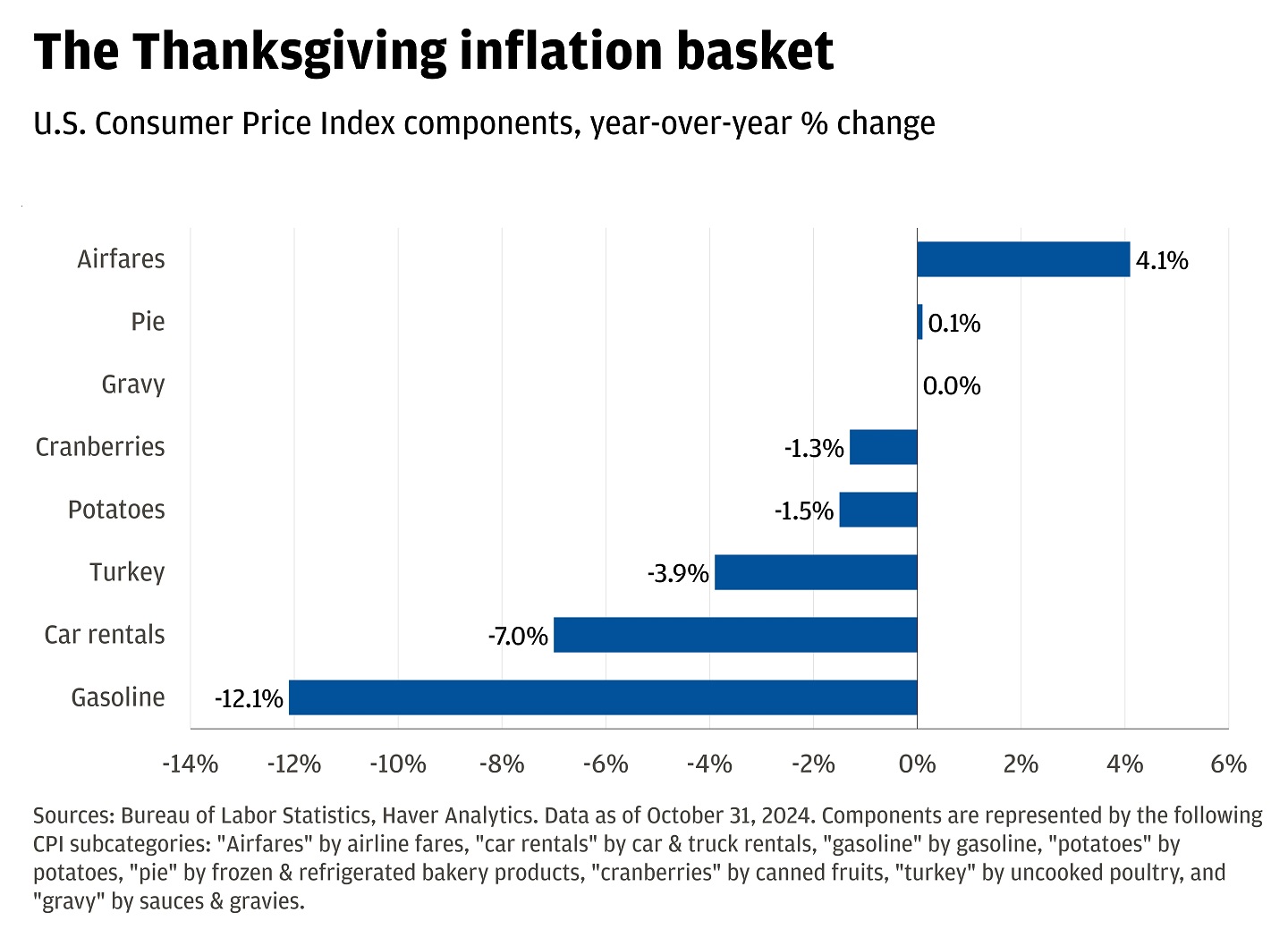

2. Cooling inflation and a sturdy labor market. One of the biggest surprises this year has been how much inflation has continued to cool against a fairly solid economic backdrop. As mentioned above, inflation is still is not fully back to the Fed’s sweet spot, but it is darn close. As prices continue to normalize, that means your Thanksgiving grocery bill and travel plans may be cheaper than last year. Compared to just a year ago, gasoline, car rentals, turkey, potatoes, cranberries and gravy prices are down meaningfully while airfares and pies are still more expensive. As the progress continues, we are especially thankful for a sturdy labor market. Over the last year real wages have grown by 2%, which is strong and the fastest pace achieved since 2015. That has given consumers a bit of relief when it comes to keeping up with price pains.

The Thanksgiving inflation basket

U.S. Consumer Price Index components, year-over-year percentage change

This bar chart shows U.S. Consumer Price Index components, year-over-year % change among airfares, pie, gravy, cranberries, potatoes, turkey, car rentals, and gasoline. For airfares, year-over-year % change was 4.1%. For pie, year-over-year % change was 0.1%. For gravy, year-over-year % change was 0%. For cranberries, year-over-year % change was -1.3%. For potatoes, year-over-year % change was -1.5%. For turkey, year-over-year % change was -3.9%. For car rentals, year-over-year % change was -7%. For gasoline, year-over-year % change was -12.1%.

Source: Bureau of Labor Statistics, Haver Analytics. Data as of October 31, 2024. Components are represented by the following CPI subcategories: "Airfares" by airline fares, "car rentals" by car & truck rentals, "gasoline" by gasoline, "potatoes" by potatoes, "pie" by frozen & refrigerated bakery products, "cranberries" by canned fruits, "turkey" by uncooked poultry, and "gravy" by sauces & gravies.

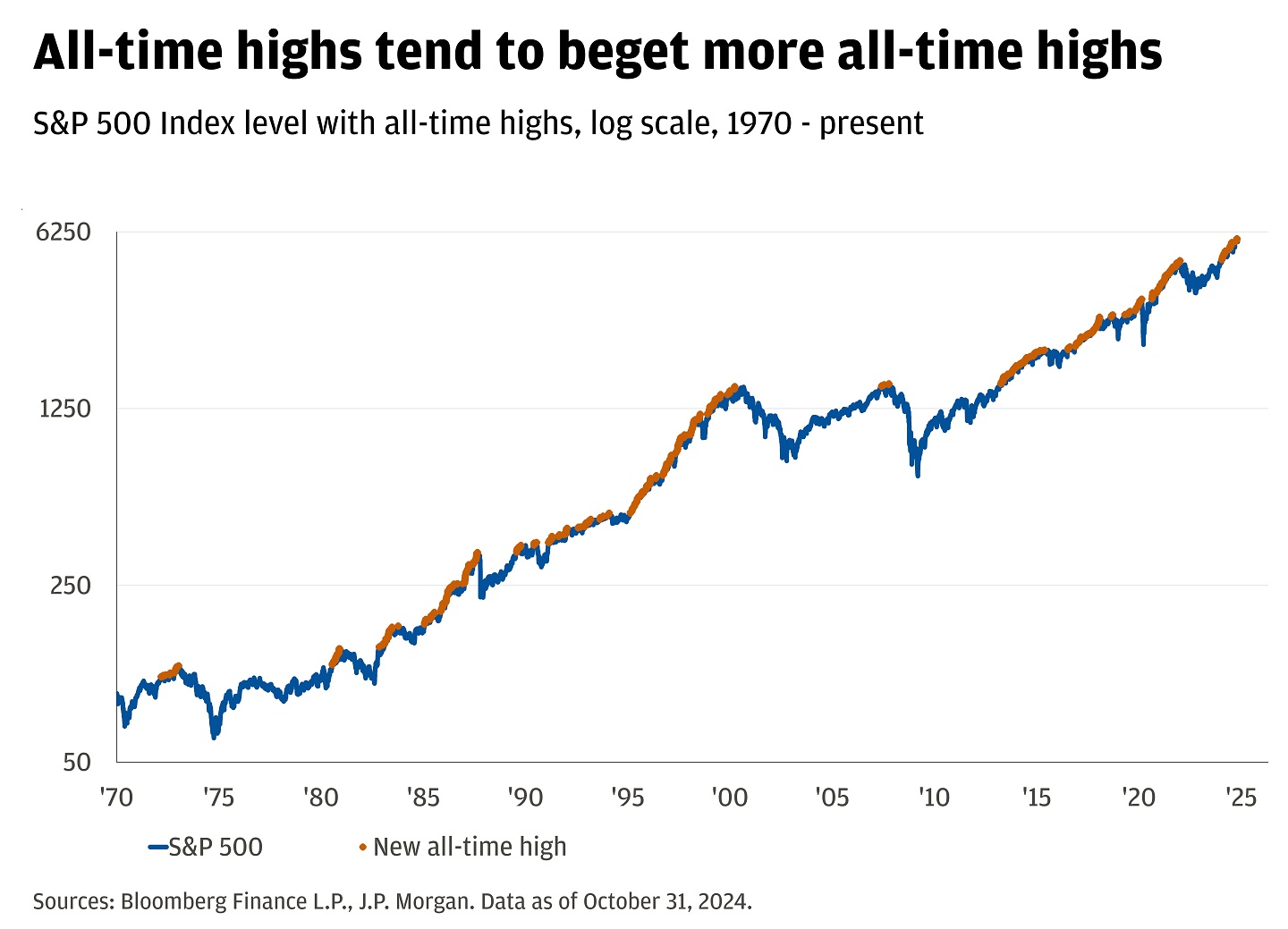

3. Over 50 all-time highs for the S&P 500. The S&P 500 has had a stellar year so far, up over 25% despite election jitters, inflation uncertainty, geopolitical tensions and elevated rates. After gaining 24% in 2023, the index is on pace for the first back-to-back years of 20%+ gains since the late 1990s. The good news is that we think the momentum can continue for a couple of key reasons:

- Earnings should continue to be supportive. This year companies were able to produce profits in the face of historically restrictive rates. Looking ahead to next year, every sector in the S&P 500 is expected to post positive earnings growth. That has not happened since 2018 and lower rates are the cherry on top.

- History looks to be on our side when it comes to the bull market. The median bull market total return is 110%. The current bull market total return is only 62% as of the end of October. In other words, if this run is merely in line with history, there looks to be upside from here.

All-time highs tend to beget more all-time highs

S&P 500 Index level with all-time highs, log scale, 1970 - present

This line chart shows the S&P 500 Index level with all-time highs on a log scale from 1970 – present, denoting points that show specific all-time highs. In 1/2/1970, the S&P Index level was 93. On 4/5/1972, there was a new all-time high of 109. On 10/1/1974, the S&P 500 index level was 63.39. On 2/17/1987, there was a new all-time high at 285.49. On 12/3/1987, the S&P 500 index level was 225.21. On 12/8/1994, the S&P 500 index level was 445.45. On 11/16/1999, there was a new all-time high of 1420.07. On 10/9/2002, the S&P 500 index level was 776.76. On 5/30/2007, there was a new all-time high at 1530.23. On 3/9/2009, the S&P 500 index level was 676.53. On 8/24/2018, there was a new all-time high at 2874.69. On 3/23/2020, the S&P 500 index level was 2237.4. On 9/19/2-24, there was a new all-time high at 5713.64.

Source: Bloomberg Finance L.P., J.P. Morgan. Data as of October 31, 2024.

We know there are a lot of reasons beyond what we mentioned to be thankful for this Thanksgiving. That said, we are particularly optimistic about the opportunity that may lie ahead. As outlined in our 2025 Outlook, we think markets are well positioned to build on 2024’s strength in years to come.

Above all though, we’re grateful for the trust that you place in all of us at J.P. Morgan, and for following markets along with us throughout the year by reading Top Market Takeaways.

Cheers, and a Happy Thanksgiving to you and yours.

All market and economic data as of 11/27/2024 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

Connect with a Wealth Advisor

Reach out to your Wealth Advisor to discuss any considerations for your current portfolio. If you don’t have a Wealth Advisor, click here to tell us about your needs and we’ll reach out to you.

DISCLOSURES

The information presented is not intended to be making value judgments on the preferred outcome of any government decision or political election.

Private investments are subject to special risks. Individuals must meet specific suitability standards before investing. This information does not constitute an offer to sell or a solicitation of an offer to buy. As a reminder, hedge funds (or funds of hedge funds), private equity funds, real estate funds often engage in leveraging and other speculative investment practices that may increase the risk of investment loss. These investments can be highly illiquid, and are not required to provide periodic pricing or valuation information to investors

Investing in fixed income products is subject to certain risks, including interest rate, credit, inflation, call, prepayment, and reinvestment risk.

The price of equity securities may rise or fall due to the changes in the broad market or changes in a company's financial condition, sometimes rapidly or unpredictably. Equity securities are subject to "stock market risk" meaning that stock prices in general may decline over short or extended periods of time.

International investments may not be suitable for all investors. International investing involves a greater degree of risk and increased volatility. Changes in currency exchange rates and differences in accounting and taxation policies outside the U.S. can raise or lower returns. Some overseas markets may not be as politically and economically stable as the United States and other nations. Investments in international markets can be more volatile.

Private Equity is typically composed of Venture Capital, Leveraged Buyouts, Distressed Investments and Mezzanine Financing, which are all generally considered to be high risk, illiquid investments designed to deliver larger expected returns than publicly traded securities as compensation for their greater risk. As a result, investing in Private Equity is not suitable for all investors.

Index definitions:

The Russell 3000 Index is a capitalization-weighted stock market index that seeks to be a benchmark of the entire U.S. stock market. It measures the performance of the largest 3,000 U.S. companies representing approximately 96% of the investable U.S. equity market.

The S&P 500 Equal Weight Index is the equal-weight version of the widely-used S&P 500. The index includes the same constituents as the capitalization weighted S&P 500, but each company in the S&P 500 EWI is allocated a fixed weight of the index total at each quarterly rebalance.

The Bloomberg U.S. Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate pass-throughs), ABS and CMBS (agency and non-agency).

The Magnificent Seven stocks are a group of influential companies in the U.S. stock market: Alphabet, Amazon, Apple, Meta Platforms, Microsoft, NVIDIA, and Tesla.

The Magnificent 7 Index is an equal-dollar weighted equity benchmark consisting of a fixed basket of 7 widely-traded companies (Microsoft, Apple, Nvidia, Alphabet, Amazon, Meta, Tesla) classified in the United States and representing the Communications, Consumer Discretionary and Technology sectors as defined by Bloomberg Industry Classification System (BICS).

The S&P Midcap 400 Index is a capitalization-weighted index which measures the performance of the mid-range sector of the U.S. stock market.

The S&P 500 index is widely regarded as the best single gauge of large-cap U.S. equities and serves as the foundation for a wide range of investment products. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization.

Bonds are subject to interest rate risk, credit, call, liquidity and default risk of the issuer. Bond prices generally fall when interest rates rise.

Standard and Poor’s 500 Index is a capitalization-weighted index of 500 stocks. The index is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The index was developed with a base level of 10 for the 1941–43 base period.

The Bloomberg Eco Surprise Index shows the degree to which economic analysts under- or over-estimate the trends in the business cycle. The surprise element is defined as the percentage difference between analyst forecasts and the published value of economic data releases.

The MSCI World Index is a free float-adjusted market capitalization index that is designed to measure global developed market equity performance.

The NASDAQ 100 Index is a basket of the 100 largest, most actively traded U.S companies listed on the NASDAQ stock exchange. The index includes companies from various industries except for the financial industry, like commercial and investment banks. These non-financial sectors include retail, biotechnology, industrial, technology, health care, and others.

The Russell 2000 Index measures small company stock market performance. The index does not include fees or expenses.

We believe the information contained in this material to be reliable but do not warrant its accuracy or completeness. Opinions, estimates, and investment strategies and views expressed in this document constitute our judgment based on current market conditions and are subject to change without notice.

The views, opinions, estimates and strategies expressed herein constitutes the author's judgment based on current market conditions and are subject to change without notice, and may differ from those expressed by other areas of J.P. Morgan. This information in no way constitutes J.P. Morgan Research and should not be treated as such. You should carefully consider your needs and objectives before making any decisions. For additional guidance on how this information should be applied to your situation, you should consult your advisor.

All companies referenced are shown for illustrative purposes only, and are not intended as a recommendation or endorsement by J.P. Morgan in this context.

JPMorgan Chase & Co., its affiliates, and employees do not provide tax, legal or accounting advice. Information presented on these webpages is not intended to provide, and should not be relied on for tax, legal and accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any financial transaction.

RISK CONSIDERATIONS

- Past performance is not indicative of future results. You may not invest directly in an index.

- The price of equity securities may rise or fall due to the changes in the broad market or changes in a company's financial condition, sometimes rapidly or unpredictably. Equity securities are subject to 'stock market risk' meaning that stock prices in general may decline over short or extended periods of time.

- Investing in fixed income products is subject to certain risks, including interest rate, credit, inflation, call, prepayment and reinvestment risk. Any fixed income security sold or redeemed prior to maturity may be subject to substantial gain or loss.

- In general, the bond market is volatile and bond prices rise when interest rates fall and vice versa. Longer term securities are more prone to price fluctuation than shorter term securities. Any fixed income security sold or redeemed prior to maturity may be subject to substantial gain or loss. Dependable income is subject to the credit risk of the issuer of the bond. If an issuer defaults no future income payments will be made.

- When investing in mutual funds or exchange-traded and index funds, please consider the investment objectives, risks, charges, and expenses associated with the funds before investing. You may obtain a fund’s prospectus by contacting your investment professional. The prospectus contains information, which should be carefully read before investing.

- Investors should understand the potential tax liabilities surrounding a municipal bond purchase. Certain municipal bonds are federally taxed if the holder is subject to alternative minimum tax. Capital gains, if any, are federally taxable. The investor should note that the income from tax-free municipal bond funds may be subject to state and local taxation and the alternative minimum tax (amt).

- International investments may not be suitable for all investors. International investing involves a greater degree of risk and increased volatility. Changes in currency exchange rates and differences in accounting and taxation policies outside the U.S. can raise or lower returns. Some overseas markets may not be as politically and economically stable as the united states and other nations. Investments in international markets can be more volatile.

- Investments in emerging markets may not be suitable for all investors. Emerging markets involve a greater degree of risk and increased volatility. Changes in currency exchange rates and differences in accounting and taxation policies outside the U.S. can raise or lower returns. Some overseas markets may not be as politically and economically stable as the united states and other nations. Investments in emerging markets can be more volatile.

- Investments in commodities may have greater volatility than investments in traditional securities, particularly if the instruments involve leverage. The value of commodity-linked derivative instruments may be affected by changes in overall market movements, commodity index volatility, changes in interest rates, or factors affecting a particular industry or commodity, such as drought, floods, weather, livestock disease, embargoes, tariffs and international economic, political and regulatory developments. Use of leveraged commodity-linked derivatives creates an opportunity for increased return but, at the same time, creates the possibility for greater loss.

- Real estate investments trusts may be subject to a high degree of market risk because of concentration in a specific industry, sector or geographical sector. Real estate investments may be subject to risks including, but not limited to, declines in the value of real estate, risks related to general and economic conditions, changes in the value of the underlying property owned by the trust and defaults by borrower.

- Investment in alternative investment strategies is speculative, often involves a greater degree of risk than traditional investments including limited liquidity and limited transparency, among other factors and should only be considered by sophisticated investors with the financial capability to accept the loss of all or part of the assets devoted to such strategies.

- Structured products involve derivatives and risks that may not be suitable for all investors. The most common risks include, but are not limited to, risk of adverse or unanticipated market developments, issuer credit quality risk, risk of lack of uniform standard pricing, risk of adverse events involving any underlying reference obligations, risk of high volatility, risk of illiquidity/little to no secondary market, and conflicts of interest. Before investing in a structured product, investors should review the accompanying offering document, prospectus or prospectus supplement to understand the actual terms and key risks associated with the each individual structured product. Any payments on a structured product are subject to the credit risk of the issuer and/or guarantor. Investors may lose their entire investment, i.e., incur an unlimited loss. The risks listed above are not complete. For a more comprehensive list of the risks involved with this particular product, please speak to your J.P. Morgan team.

- As a reminder, hedge funds (or funds of hedge funds) often engage in leveraging and other speculative investment practices that may increase the risk of investment loss. These investments can be highly illiquid, and are not required to provide periodic pricing or valuation information to investors, and may involve complex tax structures and delays in distributing important tax information. These investments are not subject to the same regulatory requirements as mutual funds; and often charge high fees. Further, any number of conflicts of interest may exist in the context of the management and/or operation of any such fund. For complete information, please refer to the applicable offering memorandum.

- For informational purposes only -- J.P. Morgan Securities LLC does not endorse, advise on, transmit, sell or transact in any type of virtual currency. Please note: J.P. Morgan Securities LLC does not intermediate, mine, transmit, custody, store, sell, exchange, control, administer, or issue any type of virtual currency, which includes any type of digital unit used as a medium of exchange or a form of digitally stored value.

- The prices and rates of return are indicative, as they may vary over time based on market conditions.

- Additional risk considerations exist for all strategies.

- The information provided herein is not intended as a recommendation of or an offer or solicitation to purchase or sell any investment product or service.

- Opinions expressed herein may differ from the opinions expressed by other areas of J.P. Morgan. This material should not be regarded as investment research or a J.P. Morgan investment research report.

This material is for information purposes only, and may inform you of certain products and services offered by J.P. Morgan’s wealth management businesses, part of JPMorgan Chase & Co. (“JPM”). The views and strategies described in the material may not be suitable for all investors and are subject to investment risks. Please read all Important Information.

GENERAL RISKS & CONSIDERATIONS. Any views, strategies or products discussed in this material may not be appropriate for all individuals and are subject to risks. Investors may get back less than they invested, and past performance is not a reliable indicator of future results. Asset allocation/diversification does not guarantee a profit or protect against loss. Nothing in this material should be relied upon in isolation for the purpose of making an investment decision. You are urged to consider carefully whether the services, products, asset classes (e.g. equities, fixed income, alternative investments, commodities, etc.) or strategies discussed are suitable to your needs. You must also consider the objectives, risks, charges, and expenses associated with an investment service, product or strategy prior to making an investment decision. For this and more complete information, including discussion of your goals/situation, contact your J.P. Morgan team.

NON-RELIANCE. Certain information contained in this material is believed to be reliable; however, JPM does not represent or warrant its accuracy, reliability or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. No representation or warranty should be made with regard to any computations, graphs, tables, diagrams or commentary in this material, which are provided for illustration/reference purposes only. The views, opinions, estimates and strategies expressed in this material constitute our judgment based on current market conditions and are subject to change without notice. JPM assumes no duty to update any information in this material in the event that such information changes. Views, opinions, estimates and strategies expressed herein may differ from those expressed by other areas of JPM, views expressed for other purposes or in other contexts, and this material should not be regarded as a research report. Any projected results and risks are based solely on hypothetical examples cited, and actual results and risks will vary depending on specific circumstances. Forward-looking statements should not be considered as guarantees or predictions of future events.

Nothing in this document shall be construed as giving rise to any duty of care owed to, or advisory relationship with, you or any third party. Nothing in this document shall be regarded as an offer, solicitation, recommendation or advice (whether financial, accounting, legal, tax or other) given by J.P. Morgan and/or its officers or employees, irrespective of whether or not such communication was given at your request. J.P. Morgan and its affiliates and employees do not provide tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any financial transactions.

LEGAL ENTITY, BRAND & REGULATORY INFORMATION

In the United States, bank deposit accounts and related services, such as checking, savings and bank lending, are offered by JPMorgan Chase Bank, N.A. Member FDIC.

J.P. Morgan Wealth Management is a business of JPMorgan Chase & Co., which offers investment products and services through J.P. Morgan Securities LLC (JPMS), a registered broker-dealer and investment adviser, member FINRA and SIPC. Insurance products are made available through Chase Insurance Agency, Inc. (CIA), a licensed insurance agency, doing business as Chase Insurance Agency Services, Inc. in Florida. Certain custody and other services are provided by JPMorgan Chase Bank, N.A. (JPMCB). JPMS, CIA and JPMCB are affiliated companies under the common control of JPMorgan Chase & Co. Products not available in all states.

Bank deposit accounts and related services, such as checking, savings and bank lending, are offered by JPMorgan Chase Bank, N.A. Member FDIC.

This document may provide information about the brokerage and investment advisory services provided by J.P. Morgan Securities LLC (“JPMS”). The agreements entered into with JPMS, and corresponding disclosures provided with respect to the different products and services provided by JPMS (including our Form ADV disclosure brochure, if and when applicable), contain important information about the capacity in which we will be acting. You should read them all carefully. We encourage clients to speak to their JPMS representative regarding the nature of the products and services and to ask any questions they may have about the difference between brokerage and investment advisory services, including the obligation to disclose conflicts of interests and to act in the best interests of our clients.

J.P. Morgan may hold a position for itself or our other clients which may not be consistent with the information, opinions, estimates, investment strategies or views expressed in this document. JPMorgan Chase & Co. or its affiliates may hold a position or act as market maker in the financial instruments of any issuer discussed herein or act as an underwriter, placement agent, advisor or lender to such issuer.

Check the background of our firm and investment professionals on FINRA's BrokerCheck

To learn more about J. P. Morgan Wealth Management’s investment business, including our accounts, products and services, as well as our relationship with you, please review our J.P. Morgan Securities LLC Form CRS and Guide to Investment Services and Brokerage Products.

This website is for informational purposes only, and not an offer, recommendation or solicitation of any product, strategy service or transaction. Any views, strategies or products discussed on this site may not be appropriate or suitable for all individuals and are subject to risks. Prior to making any investment or financial decisions, an investor should seek individualized advice from a personal financial, legal, tax and other professional advisors that take into account all of the particular facts and circumstances of an investor's own situation.

This website may provide information about the brokerage and investment advisory services provided by J.P. Morgan Securities LLC ("JPMS"). When JPMS acts as a broker-dealer, a client's relationship with us and our duties to the client will be different in some important ways than a client's relationship with us and our duties to the client when we are acting as an investment advisor. A client should carefully read the agreements and disclosures received (including our Form ADV disclosure brochure, if and when applicable) in connection with our provision of services for important information about the capacity in which we will be acting.

INVESTMENT AND INSURANCE PRODUCTS ARE:

• NOT FDIC INSURED • NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY • NOT A DEPOSIT OR OTHER OBLIGATION OF, OR GUARANTEED BY, JPMORGAN CHASE BANK, N.A. OR ANY OF ITS AFFILIATES • SUBJECT TO INVESTMENT RISKS, INCLUDING POSSIBLE LOSS OF THE PRINCIPAL AMOUNT INVESTED

J.P. Morgan Wealth Management is a business of JPMorgan Chase & Co., which offers investment products and services through J.P. Morgan Securities LLC (JPMS), a registered broker-dealer and investment adviser, member FINRA and SIPC Insurance products are made available through Chase Insurance Agency, Inc. (CIA), a licensed insurance agency, doing business as Chase Insurance Agency Services, Inc. in Florida. Certain custody and other services are provided by JPMorgan Chase Bank, N.A. (JPMCB). JPMS, CIA and JPMCB are affiliated companies under the common control of JPMorgan Chase & Co. Products not available in all states.

Please read additional Important Information in conjunction with these pages.